annotation

L'apprentissage automatique joue un rôle important dans la prévention des pertes financières dans le secteur bancaire. Le défi le plus pressant en matière de prévisions est peut-être l'évaluation du risque de crédit (le risque de défaut de paiement). De tels risques peuvent entraîner des pertes de milliards de dollars par an. Aujourd'hui, la plupart des avantages de l'apprentissage automatique dans la prédiction du risque de crédit sont dus aux modèles d'arbre de décision d'amélioration du gradient. Cependant, ces avantages commencent à diminuer s'ils ne sont pas pris en charge par de nouvelles sources de données et / ou des fonctionnalités flexibles de haute technologie. Dans cet article, nous présentons nos tentatives pour créer une nouvelle approche de l'évaluation du risque de crédit en utilisant un apprentissage en profondeur qui n'implique pas de surveillance complexe, ne repose pas sur de nouvelles entrées de modèle.Nous proposons de nouvelles méthodes pour récupérer les transactions par carte de crédit à utiliser avec des réseaux de neurones convolutifs récurrents et causaux profonds qui utilisent des séquences temporelles de données financières, sans besoins de ressources spécifiques. Nous montrons que notre approche séquentielle de l'apprentissage profond utilisant un réseau convolutif temporaire a surpassé le modèle d'arbre incohérent de référence, réalisant des économies financières importantes et une détection précoce du risque de crédit. Nous démontrons également le potentiel de notre approche pour une utilisation dans un environnement de production, où la technique d'échantillonnage proposée permet un stockage efficace des séquences en mémoire, en les utilisant pour une formation et une production en ligne rapides.qui utilisent des séquences temporelles de données financières, sans besoins particuliers en ressources. Nous montrons que notre approche séquentielle de l'apprentissage profond utilisant un réseau convolutif temporaire a surpassé le modèle d'arbre incohérent de référence, réalisant des économies financières importantes et une détection précoce du risque de crédit. Nous démontrons également le potentiel de notre approche pour une utilisation dans un environnement de production, où la technique d'échantillonnage proposée permet un stockage efficace des séquences en mémoire, en les utilisant pour une formation et une production en ligne rapides.qui utilisent des séquences temporelles de données financières, sans besoins particuliers en ressources. Nous montrons que notre approche séquentielle de l'apprentissage profond utilisant un réseau convolutif temporaire a surpassé le modèle d'arbre incohérent de référence, réalisant des économies financières importantes et une détection précoce du risque de crédit. Nous démontrons également le potentiel de notre approche pour une utilisation dans un environnement de production, où la technique d'échantillonnage proposée permet un stockage efficace des séquences en mémoire, en les utilisant pour une formation et une production en ligne rapides.avoir réalisé d'importantes économies financières et une détection précoce du risque de crédit. Nous démontrons également le potentiel de notre approche pour une utilisation dans un environnement de production, où la technique d'échantillonnage proposée permet un stockage efficace des séquences en mémoire, en les utilisant pour une formation et une production en ligne rapides.avoir réalisé d'importantes économies financières et une détection précoce du risque de crédit. Nous démontrons également le potentiel de notre approche pour une utilisation dans un environnement de production, où la technique d'échantillonnage proposée permet un stockage efficace des séquences en mémoire, en les utilisant pour une formation et une production en ligne rapides.

KEYWORDS credit risk, tabular data, credit card transactions, recurrent neural networks, temporal convolutional networks

1.

, , , (, ). , [24].

(GBDTs), , [10]. , . , , , , . . -, , . -, . , - ( ) - , , (, [6]).

, , . , GBDT, , (TCN) . , , . - .

[9, 23], [3, 26] [1,19]. , , (RNN) TCN, . , , . , , , « » , / . , , -. - .

, , . , ( ) -. , . , , - .

2.

2.1.

, . , () 1,5 .

2.1.1. . . , , , () , 127 . : ( , . .) ( , . .). , . - .

2.1.2. . 15 , 2016 2017 . , 45 . , ( ) .

6 ( ) , 2017 2018 , . , . 2% . , - - , - , .

2.1.3. . , , . , . :

( / ) 10 , ;

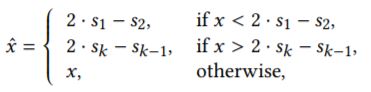

«» , , , ( GBDT), , , : (s1, s2, . . . , sk ), si > sj , for all i > j, :

x - , xˆ- ( . . 1);

• - [5];

• () , [18] :

;

1, :

G - , | G | - , k – -, ( k = 30), y - .

• , .

2.2.

. . , , - . , , , .

– . -, , - . -, , 11 . ( . 2). , ( 10 ).

. , – , , . , .

12 , . .

2.3.

, , GBDT . GBDT , . , ( TabNet) .

2.3.1 . (MLP) . MLP / . "" , MLP [13]. , , , .

2.3.2. TabNet. TabNet - , [2]. , . TabNet : . , . , , , (. 3). , , .

2.3.3. . , GBDT: . RNNS , .

long short-term memory (LSTM) RNN [14], RNN. , . RNN, zoneout [17]. , zoneout RNN. , , zoneout . zoneout , RNN . LSTM zoneout .4.

basée sur des données de transaction sur 12 mois.")

2.3.4 . RNN , , . , RNN [21]. , [4, 7, 11, 15, 20]. , , , RNNs. , . , t t (. . 5) [25].

, , , (TCN) [4]. , TCNS (), , , [27]. TCNS , , (. . 6), [12]. TCN , . deep TCN . 7.

2.4.

2.4.1. . , /, , SigOpt [8]. , - . , 5- MLP, 3- LSTM ( 2 LSTM ) 6- TCN ( 2 TCN 4 ). ( ~0,2).

2.4.2. . [16] [22]. - ( = 0,9, 0,999), , . - , .

2.4.3. . , . , 512 0,8, 1e-4, , .

2.4.4 . . , . ( = (2*AUROC) - 1). , , - . - .

3.

GBDT 1. ( 15 000 ) , .

")

, LSTM TCN, GBDT. MLP TabNet . , , LSTM TCN GBDT, , , . , , , , ( ).

3.1. . , , . , , .

LSTM TCN GBDT ( , , ) 2. , GBDT, -, ( 6 ), , , ( 7-12 ) ( 13-18 ), , .

3.2. . ( ). 8 , , , , , « » , . LSTM, TCN 12 , TCN LSTM . , , . , 2016 .

3.3. -. , , LSTM TCN -. , , 2017 . . 9, . , , . , .

a donné de meilleurs résultats de performance par rapport à la réinitialisation des pondérations avec de petites valeurs aléatoires avant l'entraînement.")

3.4. . TCN LSTM , . NVDIA Tesla V100, ~30 , TCN - 512 , ~50 LSTM. , TCN , , LSTM.

, LSTM , TCN. Bai et al. [4], LSTM / , . , TCN . , 1 , , ( 10 ). , , , , (TCN) (LSTM).

4. .

, , , . .

, . , TCN . , , -.

, , LSTM TCN. , GBDT , . , - ( ) .

- , , , , . , , . , .

[1] Peter Martey Addo, Dominique Guegan, and Bertrand Hassani. 2018. Credit

risk analysis using machine and deep learning models. Risks 6, 2 (2018), 38.

https://doi.org/10.3390/risks6020038

[2] Sercan O. Arik and Tomas Pfister. 2019. TabNet: Attentive Interpretable Tabular

Learning. (2019). arXiv:1908.07442

[3] Dmitrii Babaev, Alexander Tuzhilin, Maxim Savchenko, and Dmitrii Umerenkov. E.T.-Rnn: Applying deep learning to credit loan applications. In Proceedings of the ACM SIGKDD International Conference on Knowledge Discovery and Data Mining. 2183–2190. https://doi.org/10.1145/3292500.3330693

[4] Shaojie Bai, J. Zico Kolter, and Vladlen Koltun. 2018. An Empirical Evaluation of Generic Convolutional and Recurrent Networks for Sequence Modeling. (2018). arXiv:1803.01271

[5] George EP Box and David R Cox. 1964. An analysis of transformations. Journal of the Royal Statistical Society: Series B (Methodological) 26, 2 (1964), 211–243.

[6] Tianqi Chen and Carlos Guestrin. 2016. Xgboost: A scalable tree boosting system. In Proceedings of the 22nd ACM SIGKDD Unternational Conference on Knowledge Discovery and Data Mining. 785–794.

[7] Yann N Dauphin, Angela Fan, Michael Auli, and David Grangier. 2017. Language modeling with gated convolutional networks. In Proceedings of the 34th International Conference on Machine Learning. 933–941.

[8] Ian Dewancker, Michael McCourt, and Scott Clark. 2015. Bayesian Optimization Primer.

[9] Dmitry Efimov, Di Xu, Alexey Nefedov, and Archana Anandakrishnan. 2019. Using Generative Adversarial Networks to Synthesize Artificial Financial Datasets. In 33rd Conference on Neural Information Processing Systems, Workshop on Robust AI in Financial Services.

[10] Jerome H. Friedman. 2001. Greedy function approximation: A gradient boosting machine. Annals of Statistics 29, 5 (2001), 1189–1232. https://doi.org/10.2307/ 2699986

[11] Jonas Gehring, Michael Auli, David Grangier, Denis Yarats, and Yann N Dauphin. Convolutional sequence to sequence learning. In Proceedings of the 34th International Conference on Machine Learning. 1243–1252.

[12] Kaiming He, Xiangyu Zhang, Shaoqing Ren, and Jian Sun. 2016. Identity mappings in deep residual networks, Vol. 9908 LNCS. Springer Verlag, 630–645. https://doi.org/10.1007/978-3-319-46493-0_38 arXiv:1603.05027

[13] Geoffrey E Hinton, Nitish Srivastava, Alex Krizhevsky, Ilya Sutskever, and Ruslan R Salakhutdinov. 2012. Improving neural networks by preventing coadaptation of feature detectors. arXiv:1207.0580 (2012).

[14] Sepp Hochreiter and Jürgen Schmidhuber. 1997. Long Short-Term Memory. Neural Computation 9, 8 (1997), 1735–1780. https://doi.org/10.1162/neco.1997.9. 8.1735

[15] Nal Kalchbrenner, Lasse Espeholt, Karen Simonyan, Aaron van den Oord, Alex Graves, and Koray Kavukcuoglu. 2016. Neural machine translation in linear time. arXiv preprint arXiv:1610.10099 (2016).

[16] Diederik P Kingma and Jimmy Ba. 2014. Adam: A method for stochastic optimization. arXiv preprint arXiv:1412.6980 (2014).

[17] David Krueger, Tegan Maharaj, János Kramár, Mohammad Pezeshki, Nicolas Ballas, Nan Rosemary Ke, Anirudh Goyal, Yoshua Bengio, Aaron Courville, and Chris Pal. 2017. Zoneout: Regularizing rnns by randomly preserving hidden activations. In Proceedings of the 5th International Conference on Learning Representations. arXiv:1606.01305

[18] Christopher D Manning, Prabhakar Raghavan, and Hinrich Schütze. 2008. Introduction to information retrieval. Cambridge University Press. 234–265 pages.

[19] Loris Nanni and Alessandra Lumini. 2009. An experimental comparison of ensemble of classifiers for bankruptcy prediction and credit scoring. Expert Systems with Applications 36, 2 (2009), 3028–3033. https://doi.org/10.1016/j.eswa. 2008.01.018

[20] Aaron van den Oord, Sander Dieleman, Heiga Zen, Karen Simonyan, Oriol Vinyals, Alex Graves, Nal Kalchbrenner, Andrew Senior, and Koray Kavukcuoglu. Wavenet: A generative model for raw audio. arXiv preprint arXiv:1609.03499 (2016).

[21] Razvan Pascanu, Tomas Mikolov, and Yoshua Bengio. 2013. On the difficulty of training recurrent neural networks. In Proceedings of the 30th International Conference on Machine Learning. 1310–1318.

[22] Lutz Prechelt. 1998. Early stopping-but when? In Neural Networks: Tricks of the trade. Springer, 55–69.

[23] Abhimanyu Roy, Jingyi Sun, Robert Mahoney, Loreto Alonzi, Stephen Adams, and Peter Beling. 2018. Deep learning detecting fraud in credit card transactions. In Proceedings of the Systems and Information Engineering Design Symposium,129–134. https://doi.org/10.1109/SIEDS.2018.8374722

[24] Lyn C Thomas, David B Edelman, and Jonathan N Crook. 2002. Credit scoring and its applications. SIAM.

[25] Alex Waibel, Toshiyuki Hanazawa, Geoffrey Hinton, Kiyohiro Shikano, and Kevin J Lang. 1989. Phoneme recognition using time-delay neural networks. IEEE transactions on acoustics, speech, and signal processing 37, 3 (1989), 328–339.

[26] Chongren Wang, Dongmei Han, Qigang Liu et Suyuan Luo. 2018. Une approche d'apprentissage en profondeur pour la notation de crédit des prêts entre pairs à l'aide du mécanisme d'attention LSTM. Accès IEEE 7 (2018), 2161-2168.

[27] Fisher Yu et Vladlen Koltun. 2016. Agrégation de contexte multi-échelles par circonvolutions dilatées. Dans les actes de la 4e Conférence internationale sur les représentations d'apprentissage. arXiv: 1511.07122